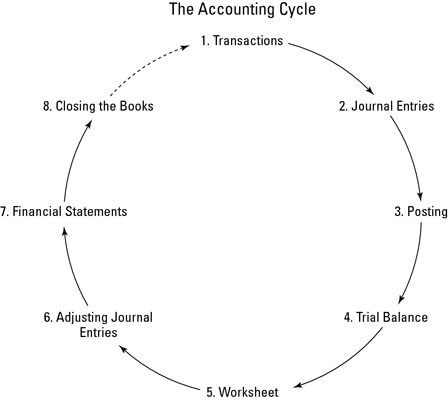

Accounting standards are needed so that financial statements will fairly and consistently describe financial performance. Without standards, users of financial statements would need to learn the accounting rules of each company, and comparisons between companies would be difficult.

Accounting standards used today are referred to as Generally Accepted Accounting Principles (GAAP). These principles are "generally accepted" because an authoritative body has set them or the accounting profession widely accepts them as appropriate.

Securities and Exchange Commission (SEC)

The Securities and Exchange Commission is a U.S. regulatory agency that has the authority to establish accounting standards for

publicly traded companies.

The Securities Act of 1933 and the Securities Exchange Act of 1934 require certain reports to be filed with the SEC.

For example, Forms 10-Q and 10-K must be filed quarterly and annually, respectively.

The head of the SEC is appointed by the President of the United States.

When the SEC was formed there was no standards-issuing body.

However, rather than set standards, the SEC encouraged the private sector to set them.

The SEC has stated that FASB standards are considered to have authoritative support.

Committee on Accounting Procedure (CAP)

In 1939, encouraged by the SEC, the American Institute of Certified Public Accountants (AICPA) formed the Committee on Accounting Procedure (CAP).

From 1939 to 1959, CAP issued 51 Accounting Research Bulletins that dealt with issues as they arose.

Accounting standards used today are referred to as Generally Accepted Accounting Principles (GAAP). These principles are "generally accepted" because an authoritative body has set them or the accounting profession widely accepts them as appropriate.

Securities and Exchange Commission (SEC)

The Securities and Exchange Commission is a U.S. regulatory agency that has the authority to establish accounting standards for

publicly traded companies.

The Securities Act of 1933 and the Securities Exchange Act of 1934 require certain reports to be filed with the SEC.

For example, Forms 10-Q and 10-K must be filed quarterly and annually, respectively.

The head of the SEC is appointed by the President of the United States.

When the SEC was formed there was no standards-issuing body.

However, rather than set standards, the SEC encouraged the private sector to set them.

The SEC has stated that FASB standards are considered to have authoritative support.

Committee on Accounting Procedure (CAP)

In 1939, encouraged by the SEC, the American Institute of Certified Public Accountants (AICPA) formed the Committee on Accounting Procedure (CAP).

From 1939 to 1959, CAP issued 51 Accounting Research Bulletins that dealt with issues as they arose.